LEASE ACCOUNTING TRENDS IN CINCINNATI

Has your company begun the transition to the new lease accounting standard?

| Cincinnati | U.S. | |

|---|---|---|

| Yes | 26% | 44% |

| No | 75% | 56% |

Finance leaders who reported their company has begun the transition also were asked: As part of that transition, have you begun the diagnostic work necessary to determine the level of effort which wil be required for you to be ready to adopt the new standard?

| Cincinnati | U.S. | |

|---|---|---|

| Yes, already completed | 23% | 48% |

| Yes, started but not completed | 77% | 51% |

| No, haven’t started | 0% | 1% |

Have you completed the following?

| Cincinnati | U.S. | |

|---|---|---|

| Identified team members and responsibilities for completing the transition to a new standard | 47% | 61% |

| Made an inventory of, and prioritized, any systems changes which might be required | 44% | 51% |

| Developed a project plan to address all gaps emanating from the diagnostic work | 38% | 49% |

| Identified, at a high level, the magnitude and type of the lease inventory (e.g., property, equipment) | 37% | 49% |

| Written new accounting policies | 65% | 47% |

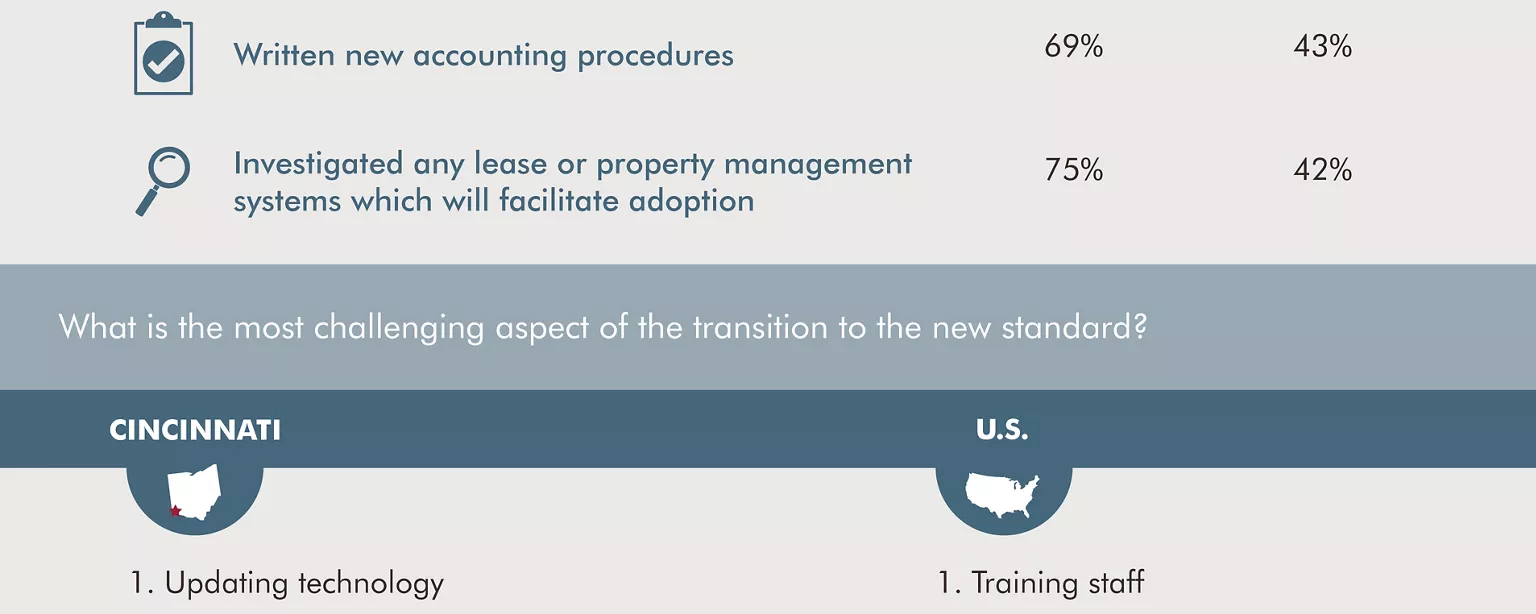

| Written new accounting procedures | 69% | 43% |

| Investigated any lease or property management systems which will facilitate adoption | 75% | 42% |

What is the most challenging aspect of the transition to the new standard?

| Cincinnati | U.S. |

|---|---|

| 1. Updating technology | 1. Training staff |

| 2. Diagnosing the needed changes | 2. Diagnosing the needed changes |

| 3. Identifying, inventorying and categorizing company’s leases | 3. Finding professionals with the requisite expertise |

For your company, which new accounting standard has been more challenging to adopt?

| Cincinnati | U.S. | |

|---|---|---|

| Revenue recognition | 84% | 71% |

| Lease accounting | 16% | 29% |

How much of the processes and learnings from transitioning to the new revenue recognition standard have you been able to apply to adopting the new lease accounting standard?

| Cincinnati | U.S. | |

|---|---|---|

| Most of them | 12% | 29% |

| Some of them | 59% | 54% |

| Almost none of them | 29% | 17% |

Source: Robert Half and Protiviti survey of more than 2,000 finance leaders in the United States, including 100 in Cincinnati

Total may not equal 100 percent due to rounding.

© 2018 Robert Half International Inc. An Equal Opportunity Employer M/F/Disability/Veterans.